Anúncios

Understanding credit costs in the UK starts with knowing how APR affects what you truly pay when borrowing money or using credit cards.

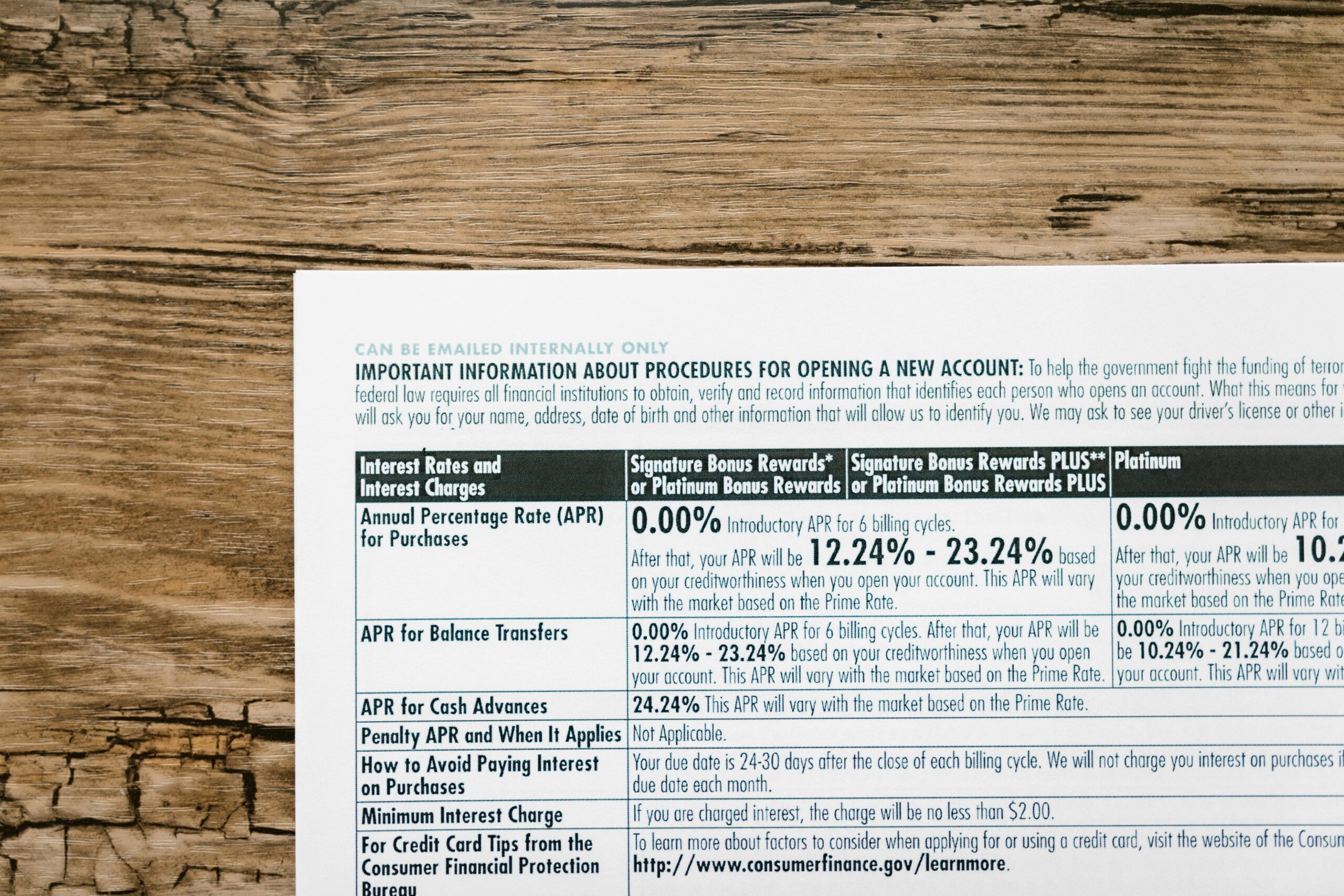

The Annual Percentage Rate, commonly referred to as APR, represents the total yearly cost of borrowing expressed as a percentage. This figure includes not just the interest charged on your balance but also mandatory fees and charges associated with the credit product. For anyone considering a credit card in the United Kingdom, grasping how APR functions is essential to making informed financial decisions.

Anúncios

Credit card rates in the UK vary considerably depending on the provider, your credit history, and the type of card you choose. Some promotional offers feature 0% introductory rates, while standard purchase APRs can range from around 20% to over 30% for those with less favourable credit profiles. Understanding these rates helps you calculate the real cost of carrying a balance and plan your repayments accordingly.

📊 What Exactly Is APR and Why Does It Matter?

APR stands for Annual Percentage Rate, a standardised metric designed to help consumers compare credit products on a level playing field. Unlike a simple interest rate, APR encompasses all compulsory costs you’ll incur over a year, including interest charges, annual fees, and other obligatory charges built into the credit agreement.

Anúncios

In the UK, lenders are legally required to display the representative APR when advertising credit products. This representative figure shows the rate that at least 51% of successful applicants will receive. However, the actual APR you’re offered may differ based on your personal credit score, income, and financial history.

For credit cards specifically, the APR tells you how much extra you’ll pay if you carry a balance from month to month. If you clear your balance in full before the payment deadline, you typically won’t pay any interest at all, making the APR irrelevant for that billing cycle. This is why understanding your payment habits is crucial when evaluating credit card offers.

💳 How Credit Card APR Works in Practice

When you use a credit card to make a purchase and don’t pay off the full balance by the due date, interest begins to accrue on the outstanding amount. The APR is divided by the number of days in the year (usually 365) to calculate a daily periodic rate. This daily rate is then applied to your outstanding balance each day.

Let’s illustrate with a practical example. Suppose your credit card has an APR of 21.9%. The daily periodic rate would be approximately 0.06% (21.9% ÷ 365). If you have a £1,000 balance, you’d be charged roughly 60 pence in interest daily. Over a month, this compounds, meaning you pay interest on the interest already added to your balance.

Different types of transactions may carry different APRs on the same card. Purchase APR applies to regular spending, while cash advance APR (often significantly higher) applies when you withdraw money from an ATM using your credit card. Balance transfer APR applies to debts moved from another card, and these rates can vary dramatically from the standard purchase rate.

🔄 The Compounding Effect on Your Balance

Interest compounds on credit cards, meaning you pay interest on previously charged interest if you don’t clear your balance. This compounding happens monthly in most UK credit card agreements. Over time, this effect can substantially increase the amount you owe, especially if you only make minimum payments.

Consider a £2,000 balance on a card with 24% APR. If you only make minimum payments of around 2-3% of the balance each month, it could take over 20 years to clear the debt, and you’d pay more than £3,000 in interest charges alone. This demonstrates why understanding APR and its long-term impact is vital for financial health.

🇬🇧 Understanding Representative APR in the UK Market

The Financial Conduct Authority (FCA) regulates how credit card companies advertise their products in the UK. The representative APR must be offered to at least 51% of successful applicants, but nearly half of accepted customers may receive a different (usually higher) rate based on their individual circumstances.

This system aims to protect consumers by providing a baseline for comparison, but it also means you cannot assume you’ll receive the advertised rate. When you apply for a credit card, the lender assesses your creditworthiness using information from credit reference agencies such as Experian, Equifax, and TransUnion.

Factors influencing your personal APR include:

- Your credit score and credit history length

- Your current income and employment status

- Existing debts and credit utilisation ratio

- Recent credit applications and hard searches

- Your residential stability and electoral roll registration

Those with excellent credit profiles may qualify for premium cards offering APRs around 18-20%, while individuals rebuilding credit might face rates exceeding 35%. Some credit-builder cards designed for those with poor credit history can carry APRs as high as 40% or more.

💷 Calculating the True Cost of Credit Card Borrowing

To understand how APR impacts your actual costs, you need to consider both the rate itself and your repayment behaviour. The total cost of credit depends on three primary factors: the APR, the amount borrowed, and the time taken to repay.

Here’s a simple comparison showing how different APRs affect the cost of borrowing £1,500 over 12 months with fixed monthly payments:

| APR | Monthly Payment | Total Repaid | Interest Paid |

|---|---|---|---|

| 18% | £137.50 | £1,650 | £150 |

| 24% | £141.80 | £1,702 | £202 |

| 30% | £146.30 | £1,756 | £256 |

| 36% | £151.00 | £1,812 | £312 |

This table demonstrates how a higher APR significantly increases your total repayment amount even over just one year. The difference between an 18% APR and a 36% APR on a £1,500 balance results in paying an extra £162 in interest over 12 months.

🧮 Using Online Calculators for Accurate Estimates

Many UK financial websites offer free credit card calculators that help you estimate repayment costs based on different APRs and payment schedules. These tools allow you to input your balance, APR, and intended monthly payment to see how long repayment will take and how much interest you’ll pay in total.

The Money Advice Service and other independent financial guidance organisations provide these calculators without bias toward any particular lender. Using these resources before committing to a credit card can help you make more informed choices about which products suit your financial situation.

🎯 Strategies to Minimise APR Impact on Your Finances

While APR is an important consideration, several practical strategies can help you minimise or completely avoid interest charges on credit cards in the UK market.

Pay Your Balance in Full: The most effective way to avoid APR costs entirely is to clear your full balance before the payment due date each month. Most UK credit cards offer an interest-free grace period of up to 56 days from the start of the billing cycle for new purchases, provided you pay the previous balance in full.

Take Advantage of 0% Promotional Periods: Many UK credit cards offer introductory 0% APR periods on purchases, balance transfers, or both. These promotional periods typically last between 6 and 29 months, during which you pay no interest on the specified transaction types. This can be a powerful tool for making large purchases or consolidating existing debt.

Consider Balance Transfer Cards: If you’re carrying expensive debt on a high-APR card, transferring the balance to a 0% balance transfer card can save hundreds or even thousands of pounds in interest. However, balance transfer fees (typically 2-4% of the transferred amount) must be factored into your calculations.

⚡ Improving Your Credit Score to Access Better Rates

Your credit score directly influences the APR you’re offered. Improving your creditworthiness can qualify you for cards with significantly lower rates, reducing your borrowing costs substantially over time.

Key actions to improve your credit profile include:

- Register on the electoral roll at your current address

- Pay all bills and credit commitments on time consistently

- Keep credit utilisation below 30% of available limits

- Avoid making multiple credit applications in short timeframes

- Check your credit reports regularly for errors and dispute inaccuracies

- Maintain older credit accounts to lengthen your credit history

Building excellent credit takes time, but the rewards include access to premium credit cards with APRs 15-20 percentage points lower than subprime offerings. This difference can translate to substantial savings if you occasionally carry a balance.

🔍 Different Types of APR You’ll Encounter

Understanding that credit cards feature multiple APRs for different transaction types helps you use these financial tools more strategically. Each APR type applies to specific circumstances and can vary significantly on the same card.

Purchase APR: This is the standard rate applied to everyday spending on your card. It’s typically the figure advertised most prominently and what people refer to when discussing a card’s APR. This rate only applies if you carry a balance beyond the interest-free grace period.

Balance Transfer APR: When you move debt from another credit card, the balance transfer APR applies. Many cards offer promotional 0% rates for balance transfers, reverting to a standard (often higher) rate after the promotional period expires. Always check what the post-promotional rate will be.

Cash Advance APR: Withdrawing cash from an ATM or obtaining cash equivalents (such as foreign currency or gambling transactions) triggers the cash advance APR, which is typically several percentage points higher than the purchase APR. Additionally, interest on cash advances usually begins accruing immediately with no grace period.

Penalty APR: Some UK credit cards may increase your APR if you miss payments or violate terms of your agreement. While less common in the UK than in other markets, it’s important to understand your card’s specific terms regarding penalty rates.

📋 How APR Relates to Other Credit Card Fees

While APR encompasses interest and certain mandatory fees, credit cards in the UK carry additional charges that aren’t included in the APR calculation but still affect your total cost of credit.

Common additional fees include:

- Late payment fees: Typically £12 for the first late payment, though some cards charge nothing for occasional missed payments

- Over-limit fees: Less common now due to regulatory changes, but some cards charge when you exceed your credit limit

- Foreign transaction fees: Usually 2.75-2.99% on purchases made in foreign currencies or outside the UK

- Cash advance fees: Typically 3-5% of the withdrawn amount, with a minimum charge of around £3

- Balance transfer fees: Generally 2-4% of the transferred balance, sometimes waived during promotional periods

These fees can add up quickly if you’re not careful about how you use your credit card. Reading the terms and conditions thoroughly before applying helps you understand the complete cost structure beyond just the APR.

🛡️ Regulatory Protections for UK Credit Card Users

The Financial Conduct Authority provides robust consumer protections for credit card users in the United Kingdom. These regulations ensure fair treatment and transparent disclosure of costs, including APR information.

Under UK law, credit card issuers must provide clear information about APRs in advertising and before you agree to a credit agreement. The pre-contract credit information document (often called the Summary Box) presents key terms including the representative APR, different APR types, fees, and other important details in a standardised, easy-to-compare format.

Additionally, Section 75 of the Consumer Credit Act provides valuable protection for purchases between £100 and £30,000 made on credit cards. This makes the card issuer jointly liable with the retailer if something goes wrong, offering an additional layer of security that can justify using a credit card for larger purchases even if you pay interest.

💡 Making Informed Decisions About Credit Card APR

Choosing a credit card shouldn’t be based solely on APR, particularly if you plan to clear your balance monthly. In that scenario, rewards, cashback, and additional benefits may offer more value than a slightly lower interest rate you’ll never pay.

However, if you anticipate carrying a balance occasionally or regularly, APR becomes a critical factor. Compare the representative APR across similar products, but also consider your likelihood of receiving that rate based on your credit profile. Using eligibility checkers offered by comparison websites can give you an indication of your approval odds without affecting your credit score.

Consider your intended use carefully. If you’re planning a large purchase and want to spread the cost, a 0% purchase card might serve better than a rewards card with a 20% APR. If you’re consolidating existing debt, a long 0% balance transfer card could save substantial sums compared to paying high interest on your current cards.

🔮 The Future of Credit Card Rates in the UK

Credit card APRs in the United Kingdom respond to various economic factors, including the Bank of England base rate, lender competition, regulatory changes, and overall credit market conditions. Understanding these broader trends helps you anticipate rate movements and time applications strategically.

When the base rate increases, credit card APRs typically follow, though not always immediately or proportionally. Conversely, base rate reductions don’t always translate to lower credit card rates, as these products price in risk premiums based on their unsecured nature.

Recent regulatory attention has focused on persistent debt, where cardholders pay more in interest and charges than they repay of their original borrowing over 18 months. New rules require card issuers to intervene and help these customers, potentially offering reduced interest rates or alternative repayment plans.

✨ Taking Control of Your Credit Card Costs

Understanding APR empowers you to make smarter choices about credit cards in the UK market. This knowledge helps you select appropriate products, use them strategically, and avoid unnecessarily expensive borrowing.

Remember that the advertised APR represents the cost of borrowing only if you carry a balance. By paying in full each month, you can enjoy credit card benefits—fraud protection, Section 75 coverage, rewards, and cashback—without paying a penny in interest regardless of the APR.

When comparing credit cards, look beyond the headline APR to understand the complete picture: promotional periods, post-promotional rates, fees for different transaction types, and additional benefits that might offset higher costs. Your personal financial habits should guide your choice more than any single metric.

Monitoring your credit score and working to improve it opens doors to better APR offers over time. Even if you currently qualify only for higher-rate cards, consistent responsible usage and timely payments can elevate your credit profile, allowing you to refinance to lower-rate products within a year or two.

The UK credit card market offers diverse products serving different needs and financial situations. Whether you’re seeking rewards on spending you’d make anyway, need breathing room to finance a large purchase, or want to consolidate existing debt, understanding how APR affects total costs enables you to match the right card to your specific circumstances without falling into expensive debt traps.