Anúncios

Interest-free credit cards have become a cornerstone of smart financial management in the UK, offering consumers valuable breathing room to manage purchases and existing debts without incurring additional costs.

Whether you’re looking to spread the cost of a significant purchase or consolidate existing credit card balances, promotional 0% interest offers can provide substantial savings when used strategically. However, understanding how these products work is essential to maximising their benefits while avoiding potential pitfalls.

Anúncios

The UK credit card market is highly competitive, with providers regularly launching attractive introductory deals to win new customers. These promotional periods can range from a few months to over two years, depending on the card and your individual creditworthiness. Let’s explore how these products function and what you need to know before applying.

🎯 Understanding 0% Interest Promotional Cards

Zero percent interest credit cards are financial products that temporarily waive interest charges on specific types of transactions. During the promotional period, you’ll pay no interest on qualifying balances, though you’ll still need to make minimum monthly payments to maintain the offer.

Anúncios

These cards typically fall into three main categories: purchase cards, balance transfer cards, and cards offering 0% on both transactions. Each serves a distinct purpose and comes with its own terms and conditions that vary significantly based on your credit profile and the lender’s assessment.

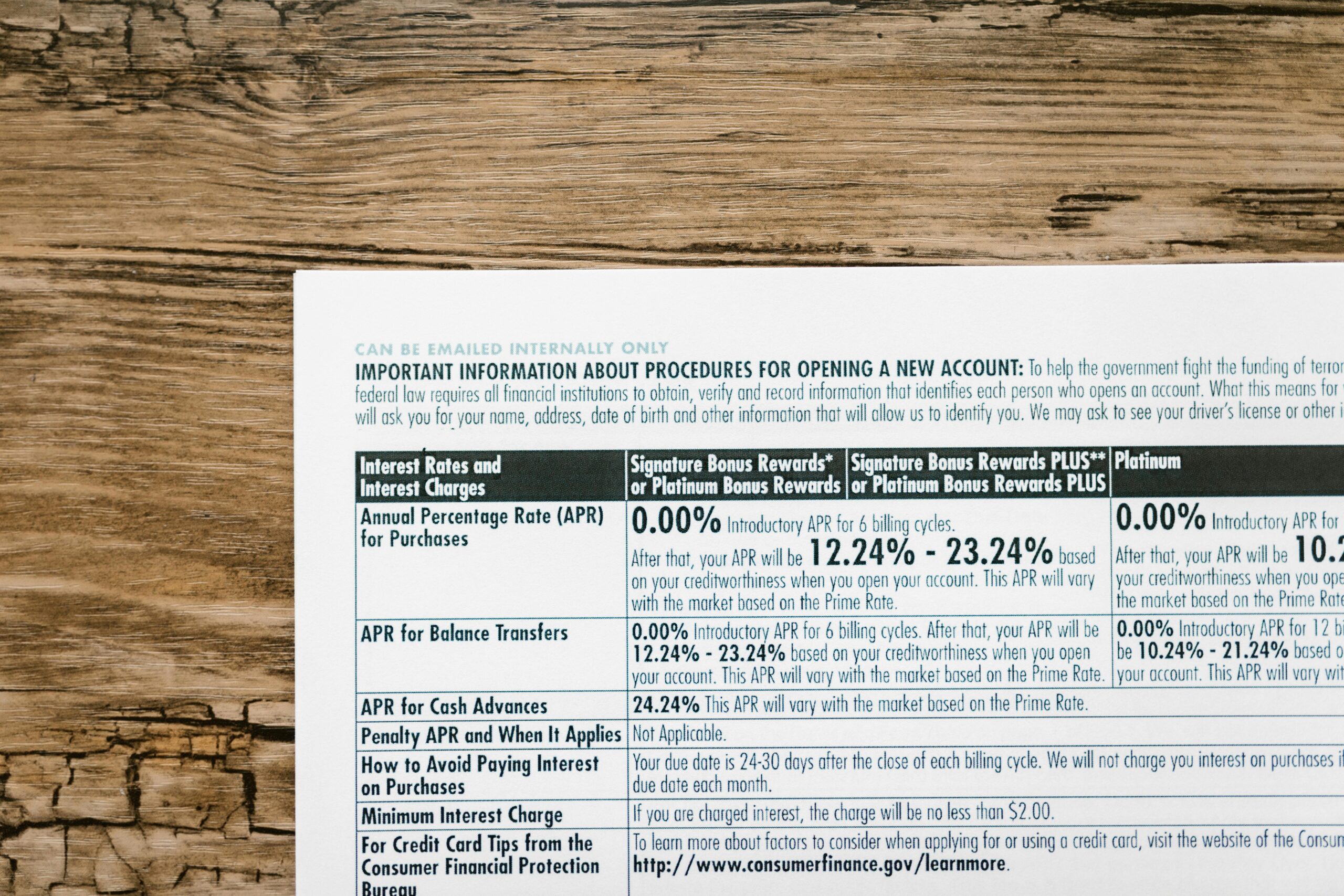

The promotional rate is introductory, meaning it applies only for a limited time. Once this period expires, a standard variable interest rate kicks in, which can be substantially higher—often ranging from 18% to 30% APR depending on your circumstances.

💳 How Purchase Cards with 0% Interest Work

Purchase cards offer interest-free periods on new spending made with the card. This makes them ideal for planned expenses like home renovations, appliances, or other significant purchases you want to spread over several months.

When you make a purchase during the promotional period, that amount won’t accrue interest until the offer ends. However, you must make at least the minimum payment each month—typically around 1-3% of your balance or a fixed minimum amount, whichever is higher.

The length of 0% purchase periods varies considerably. Some cards offer six months, while premium products might extend this to 18 months or even longer for customers with excellent credit histories. Your eligibility and the specific offer you receive depend on factors including your credit score, income, and existing financial commitments.

Strategic Use of Purchase Cards

To maximise the benefit of a 0% purchase card, plan your repayments carefully. Divide your total spending by the number of months in your promotional period to determine how much you should pay monthly to clear the balance before interest begins.

For example, if you spend £1,200 and have a 12-month interest-free period, paying £100 monthly will eliminate the debt before standard rates apply. Many cardholders set up automatic payments slightly above this calculation to account for any additional purchases or to clear the balance faster.

🔄 Balance Transfer Cards: Consolidating Existing Debt

Balance transfer cards allow you to move existing credit card debt from one or more cards to a new card offering 0% interest on transferred balances. This can result in significant savings if you’re currently paying high interest rates on existing debts.

The process involves applying for a balance transfer card and, once approved, requesting transfers from your old cards to the new one. The new provider typically pays off your old cards directly, and the balance appears on your new card under the promotional rate.

However, balance transfers aren’t free. Most providers charge a transfer fee, usually between 2-4% of the amount transferred. This upfront cost must be weighed against the interest savings you’ll achieve during the promotional period.

Calculating Balance Transfer Savings

Let’s consider a practical example. Suppose you have £3,000 spread across two credit cards charging 22% APR. Paying the minimum would keep you in debt for years and cost thousands in interest.

Transferring this balance to a card offering 28 months at 0% with a 3% transfer fee means you’d pay £90 upfront but save approximately £1,500 in interest charges if you clear the debt within the promotional period. Your monthly payment of around £110 would eliminate the debt completely before standard rates apply.

📋 Eligibility and Individual Variations

It’s crucial to understand that advertised 0% offers represent the best deals available, but not everyone who applies will receive these terms. Credit card providers in the UK use sophisticated credit scoring models to assess applications and determine individual offers.

Your credit history, income stability, existing debts, and even your address history all influence the offer you receive. Someone with an excellent credit score might qualify for 28 months at 0% on balance transfers, while another applicant might receive 15 months or be offered the card without the promotional rate at all.

Before applying, most providers offer eligibility checkers that show your likelihood of approval without affecting your credit score. These tools are invaluable for understanding what you might realistically receive before submitting a formal application.

Factors Affecting Your Offer

- Credit score: Higher scores typically unlock longer promotional periods and better terms

- Income verification: Stable, verifiable income increases approval chances and improves offers

- Existing relationship: Some banks offer preferential terms to existing customers

- Credit utilisation: Using less than 30% of your available credit across all cards demonstrates responsible management

- Recent applications: Multiple credit applications in a short period can negatively impact offers

- Address stability: Longer residential history at your current address can improve terms

⚠️ Important Limitations and Restrictions

Zero percent promotional offers come with specific terms that must be carefully observed to maintain the benefit. Failing to understand these conditions can result in losing the promotional rate entirely or accumulating charges you didn’t anticipate.

Minimum payments are mandatory every month. Missing even one payment typically voids the promotional offer, immediately reverting your balance to the standard interest rate. Additionally, late payments incur fees and damage your credit score.

Most 0% offers apply only to specific transaction types. A card offering 0% on purchases won’t extend this benefit to balance transfers or cash withdrawals, which will incur standard rates and fees from day one. Always clarify which transactions qualify for promotional rates.

Cash Advances and Other Exclusions

Cash withdrawals from ATMs or cash-equivalent transactions (like buying foreign currency or gambling) almost never qualify for promotional rates. These transactions typically incur immediate interest charges at higher rates plus withdrawal fees of around 3% or a minimum fixed fee.

Similarly, using your credit card abroad might incur foreign transaction fees, typically around 2.75-2.99% of the purchase value, even if the purchase itself qualifies for 0% interest domestically.

📊 Comparing Different 0% Card Options

The UK market offers diverse 0% credit card products, each designed for specific financial situations. Understanding the differences helps you select the most appropriate option for your circumstances.

| Card Type | Best For | Typical Duration | Key Consideration |

|---|---|---|---|

| 0% Purchase Cards | Planned spending | 6-18 months | New purchases only |

| 0% Balance Transfer | Consolidating existing debt | 18-28 months | Transfer fees apply |

| 0% Money Transfer | Cash needs or overdraft clearing | 12-18 months | Higher fees, limited availability |

| Dual 0% Cards | Purchases and transfers | 6-12 months both | Shorter periods on each |

Dual cards offering 0% on both purchases and balance transfers sound appealing but typically provide shorter promotional periods on each compared to specialist cards. Consider whether you need both benefits or if a specialist card would serve you better.

✅ Best Practices for Managing Promotional Periods

Successfully navigating a 0% promotional period requires discipline and forward planning. Creating a repayment strategy before you start using the card significantly increases your chances of clearing the balance before interest begins.

Set up a direct debit for at least the minimum payment to ensure you never miss a payment deadline. Many people go further and arrange payments that will clear the promotional balance completely before the interest-free period expires.

Keep track of when your promotional period ends by marking it clearly in your calendar with reminders set for three months, one month, and two weeks before expiry. This gives you time to either clear the remaining balance or arrange another balance transfer if necessary.

Avoiding the Promotional Period Trap

One common pitfall is treating the interest-free period as “free money” and continuing to spend without a repayment plan. Remember that every pound spent must be repaid, and when the promotional period ends, any remaining balance will incur interest at the standard rate.

Another mistake is making only minimum payments throughout the promotional period. While this keeps the 0% rate active, it means you’ll have a substantial balance remaining when standard rates begin, potentially negating much of the benefit you gained.

🔍 Understanding the Application Process

Applying for a 0% credit card involves several steps, and understanding the process helps you navigate it successfully while protecting your credit score from unnecessary damage.

Start by checking your credit report through services like Experian, Equifax, or TransUnion. Understanding your current score and correcting any errors before applying improves your chances of receiving the best available terms.

Use eligibility checkers provided by comparison websites or directly by card providers. These perform “soft searches” that don’t affect your credit score but indicate your likelihood of approval and potential offers.

When you’re ready to apply, gather necessary documentation including proof of identity, address, and income. Having these ready speeds up the application process and reduces the chance of your application being declined due to verification issues.

💡 After the Promotional Period Ends

Planning for the end of your promotional period is as important as managing it during the interest-free months. Several strategies can help you continue managing your balance effectively once standard rates apply.

If you’ve been unable to clear the balance, consider applying for another balance transfer card before your current promotion ends. This approach, sometimes called “rate surfing,” can extend your interest-free period, though it requires good credit and shouldn’t be relied upon indefinitely.

Alternatively, if your balance is manageable but not completely cleared, contact your provider to discuss your options. Some may offer promotional extensions or reduced rates to valued customers who have managed their accounts responsibly.

If neither option is available and you’ll carry a balance at standard rates, prioritise paying more than the minimum to reduce the debt quickly. Even small additional payments significantly reduce the total interest paid over time.

🎓 Regulatory Protections and Consumer Rights

UK credit card holders benefit from strong regulatory protections under the Financial Conduct Authority (FCA) rules and the Consumer Credit Act. Understanding these protections helps you use credit cards confidently and resolve issues effectively.

Section 75 of the Consumer Credit Act provides protection for purchases between £100 and £30,000, making your credit card provider jointly liable with the retailer if something goes wrong. This protection applies even during 0% promotional periods and can be invaluable for larger purchases.

If you experience financial difficulties, you have the right to contact your provider and discuss alternative arrangements. Providers are required to treat customers in financial difficulty fairly and may offer payment holidays, reduced payments, or other temporary measures.

📱 Managing Your Card Digitally

Modern credit card management happens increasingly through mobile apps and online platforms. These digital tools offer convenient ways to monitor your promotional period, track spending, and manage payments.

Most major providers offer apps that show your current balance, available credit, minimum payment due, and importantly, when your promotional period ends. Many allow you to set up custom alerts for payment due dates, approaching credit limits, or when your promotional period is nearing expiry.

Digital statements provide detailed transaction histories, making it easier to track which purchases are covered by promotional rates and which aren’t. Regularly reviewing these statements helps you stay on top of your finances and identify any unauthorised transactions quickly.

🌟 Making the Most of Your 0% Opportunity

A 0% promotional credit card represents a valuable financial tool when used strategically and managed responsibly. The key to success lies in treating the interest-free period as an opportunity to save money, not as a reason to spend more than you can afford to repay.

Before applying, clearly define your purpose. Are you consolidating expensive existing debt, planning a specific purchase, or seeking financial flexibility for anticipated expenses? Your answer should guide which type of card you choose and how you use it.

Create a realistic repayment plan before making transfers or purchases. Calculate monthly payments that will clear your balance before the promotional period ends, then set up automatic payments for this amount or higher if possible.

Finally, remember that these products work best as part of a broader financial strategy focused on reducing debt and building financial stability. Used wisely, they can save you substantial amounts in interest charges and help you achieve your financial goals faster.

The promotional credit card landscape in the UK offers genuine opportunities for savvy consumers to manage their finances more effectively. By understanding how these products work, recognising that terms vary based on individual circumstances, and approaching them with discipline and planning, you can harness their benefits while avoiding common pitfalls. Always read the specific terms and conditions of any card you’re considering, use eligibility checkers before applying, and maintain responsible repayment habits throughout your promotional period and beyond.